Timing Is Everything

Investors who got in at the right time, make good money; those that didn’t, not so much

There were two ways to make money on gaming stocks in the first half of the year:

Buy technology stocks related to sports betting.

Have the courage to buy during the Covid-19 panic of mid-March.

If you didn’t do either of those, you lost money.

Nearly every gaming company rebounded from March lows, but nearly all are well below where they began the year. Fantini’s North American Index, for example, fell 29.8 percent through June 30. Fantini’s Global Index plunged 31.8 percent. Even online stocks, so often touted as stay-at-home plays, declined. Fantini’s Interactive Index did better than its brick-and-mortar cousins but still slipped 2.4 percent.

But there were winners—big winners—if you picked the right stay-at-homes.

One place to look was Sweden. Kambi, a Stockholm-listed provider of online sports betting platforms, jumped 52 percent. Fellow Stockholm-listee Evolution Gaming, which provides live-dealer games to gambling websites, leaped 92 percent.

The U.S. had two even bigger winners. GAN, another platform provider, jumped 90 percent after its May 5 IPO. And if you were fortunate enough to get in on the IPO at $8.50, you have more than tripled your money. Draft-Kings, the daily fantasy sports operator now in the all-out gambling world, also began trading this spring. It’s up over 90 percent since its April 23 debut.

Investor infatuation with sports betting helped a couple conventional companies beat the virus, as it were. London-listed Flutter rose 12 percent in the first half. Penn National, which excited investors by purchasing a big chunk of sports media company BarStool Sports, jumped 17 percent.

Otherwise it has been red everywhere.

But not since mid-March.

For example, if you bought Wynn on January 2, you have lost 48 percent. But if you bought Wynn at its March low, you gained 73 percent by mid-year. The story is the same throughout gaming. MGM Resorts, down 50 percent for the year but up 285 percent since mid-March.

Some examples are even more extreme. Take Penn National again. The stock was $3.75 at its March low and $30.54 on June 30. That’s an eight-bagger in just over three months.

Ditto suppliers. IGT down 41 percent for the year but up 250 percent from mid-March. Little AGS down 72 percent through June and up nearly 400 percent since its low.

And those are fairly typical examples. Again, the North American Index fell 29.8 percent through June, but that’s a big comeback from mid-March, when it was down 62 percent.

The roller coaster was even steeper if you bought gaming stocks in early to mid-February when many of them hit all-time and 52-week highs.

So what does the second half of the year hold?

As Dr. Fauci might say, the virus will tell us.

If the recent explosion in Covid cases continues, or if we suffer a significant second wave in the fall, stocks could revisit the March debacle.

Even if we muddle through, there’s the reality of a high jobless rate and lost income that could mute consumer spending into next year. In such a scenario, gaming stocks today are mostly about where they should be, and could be range-bound into 2021. Another reality might sink in: casinos are not rebounding as robustly as initially, according to anecdotal reports.

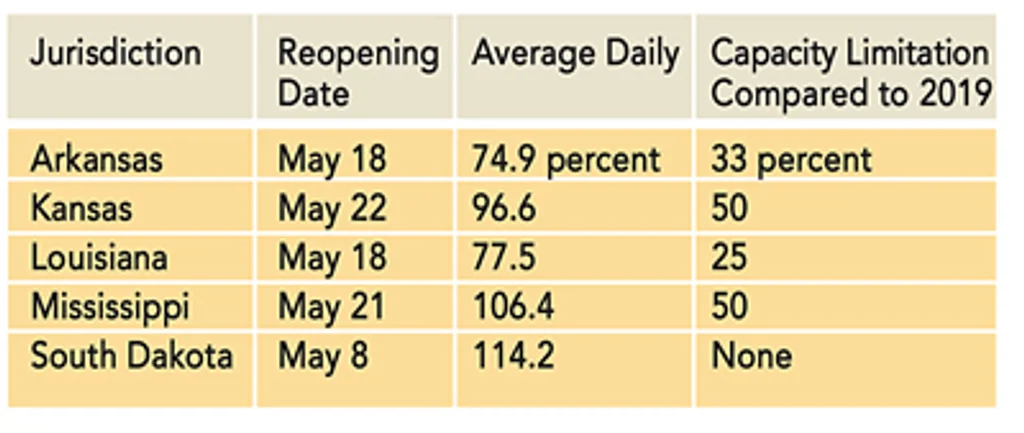

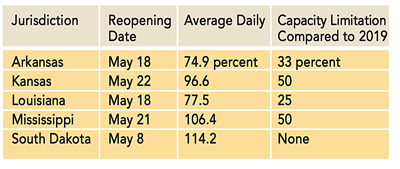

There were five states in which casinos were operating during May. Look at these gaming revenue examples from May, when the first significant jurisdictions reopened: On the surface, the numbers are encouraging with average daily revenues close to or even ahead of last year.

There were five states in which casinos were operating during May. Look at these gaming revenue examples from May, when the first significant jurisdictions reopened: On the surface, the numbers are encouraging with average daily revenues close to or even ahead of last year.

However, this represents some pent-up demand that should wane in following weeks, and a lack of many competing forms of entertainment.

It also doesn’t include non-gaming revenues lost as amenities have not reopened, or as they operate with restrictions even more stringent than those imposed on casino floors.

On the other hand, casino-deprived players are definitely going online. Here are some other numbers taken from Fantini’s National Revenue Report for May:

iGaming revenue nearly tripled to $142.9 million in the absence of many land-based gaming options and a lack of sports to bet on.

iGaming revenue nearly tripled to $142.9 million in the absence of many land-based gaming options and a lack of sports to bet on.

The steady progression of month-to-month growth is pretty obvious. The questions are whether growth will stick with brick-and-mortar casinos now open and whether enough states will legalize iGaming to have a big impact on gaming companies, whether land-based or digital.

That still leaves open the question of what the balance of the year will look like economically, in the gaming industry and in investor response.

From here, we’ll bet on muddling through to 2021 and then valuing stocks on an expected return to normality in 2022. But we won’t bet much.