Casino Life Cycles

A question that comes up often for brick-and-mortar operators is, “Where can we invest to grow gaming revenue?”

Before answering this question, it’s helpful to put it in context. The gaming landscape has changed considerably over the last several years. The brick-and-mortar casino industry started out as a scarce product in remote locales, with significant barriers to entry.

For a time, Atlantic City and later Connecticut casinos ruled the Eastern seaboard, while Las Vegas was the king of the fly-in market. Growing revenue was simply a function of adding investment. More hotel rooms, more entertainment options, more of everything. Build it and they will come.

The explosive growth of tribal and regional commercial gaming from the late 1980s through the last decade flipped this model on its head. Rising competition cut into the revenue and profits of Atlantic City casinos and the two tribal facilities in Connecticut. Facilities built for a previous era were no longer generating the free cash flow for which they were designed.

Defensive investments never brought significant returns. Revenue continued to decline. And in Atlantic City, several properties closed, one was redeveloped with transformational investment, and the newest property saw its original investment written down to a fraction of its cost before reopening.

In Las Vegas, transformational investment stemmed the tide and grew the market. But older properties eventually met their fate, and the wrecking ball and well-placed explosives sealed it. A bigger picture emerged, because at some point a casino comes to the end of its useful life and must either be imploded, reimagined or restructured and milked for every drop of cash flow.

Fast forward to today. As regional casinos mature and age, these patterns are sorting themselves out again. And as new forms of competition emerge, the patterns are hastening.

Today’s mature casinos are facing an onslaught of new competition, and the industry is being wholly disrupted. New brick-and-mortar jurisdictions or new licenses in existing jurisdictions, distributed gaming, online casinos, mobile sports betting, sweepstakes, prediction markets—the list of new competitive threats seems to be endless. And more changes are coming fast.

The Plateau

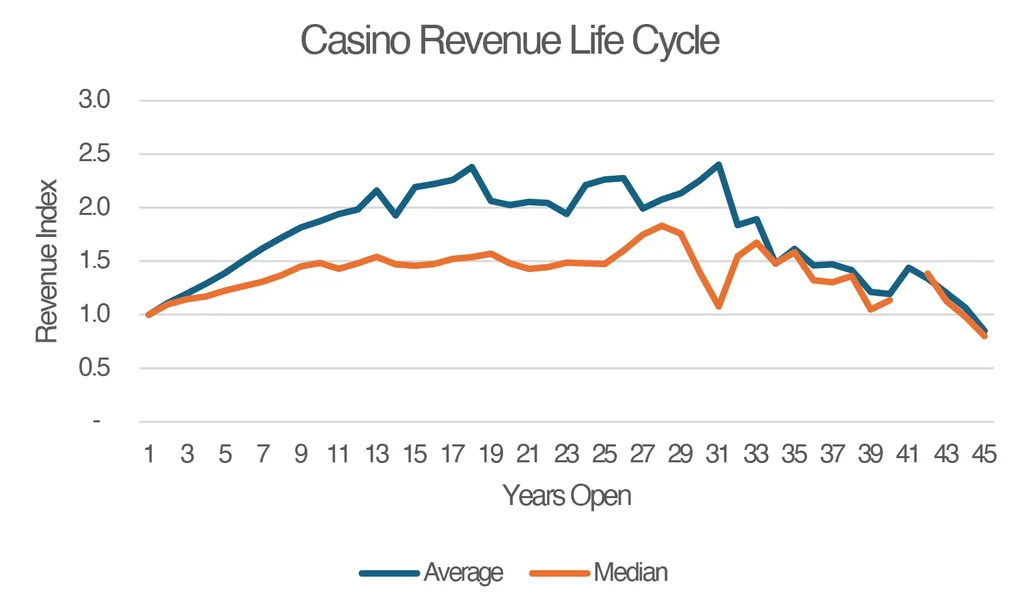

With this backdrop, gaming advisory firm GGHM studied 126 commercial casinos in several states, posing this existential question: “Where can a brick-and-mortar casino invest to grow revenue?” The answer, as usual, is… it depends. The chart on the following page depicts the average and median path for those 126 casinos, and a pattern emerges.

Casinos reach maturity at about 13 years (making me fondly recall my own bar mitzvah, though there was certainly way more growth after that event, thankfully). From the 13th through the 33rd year of operations, growth as represented by the index of revenues compared to the first full calendar year of operations is choppy, but relatively flat.

As with any set of data, applying it to a particular casino can be dicey, especially if the data you’re relying on has significant variability, and that is partially the case here. The average was dragged upward either by casinos that underwent transformative redevelopment or, in some cases, casinos that were impacted positively by economic factors such as the post-Covid stimulus. Also missing from the analysis are casinos that closed.

New brick-and-mortar jurisdictions or new licenses in existing jurisdictions, distributed gaming, online casinos, mobile sports betting, sweepstakes, prediction markets—the list of new competitive threats seems to be endless. And more changes are coming fast.

One simple observation: This looks like a typical product life cycle curve. Introduction, growth, maturity, renewal and decline. Many casinos today are nearing the end of their mature phase, and possibly their useful life. The question is whether significant capital investment is warranted. As usual, it’s market- and casino-dependent. But it’s a fair question.

Casinos are not alone in this dilemma. Mall, stadium and meeting and exhibition operators are all facing similar issues and questions, and several are facing the wrecking ball. Is that a legitimate option for casino operators?

In retail, several large malls have closed for good, and some have been redeveloped or reimagined. Examples of malls that have closed include the San Francisco Centre, which was impacted by a downtown office exodus, public safety concerns and a shift away from enclosed luxury malls.

The Forest Fair Mall/Cincinnati Mills mall closed due to an overbuilt retail market, a poor location, owner financial instability and increasing competition from newer lifestyle centers.

Many malls have been redeveloped or reimagined into larger, multi-use projects. The common factors behind the decline of malls include changing consumer behavior (walkable districts, experiential shopping, open-air versus enclosed mall) and a largely overbuilt retail sector. A good example is Tysons Corner in Virginia. The mall evolved over time from a pure retail space into a regional mixed-use hub with office, housing, residential and dining. There are clearly some parallels to the casino industry.

Sizing Up the Landscape

As casinos evaluate their unique operations and where they are in their life cycle, there are a few key considerations they should keep in mind when considering ways to maintain market relevance and positive performance:

1. Market factors. Is the market becoming more competitive? Is the new competition in-market or in a catchment area where it will be a more convenient alternative? Is local competition weak or formidable? Is there unmet demand in the market? Essentially, is the market growing, stagnant or potentially in decline? The case for investment is certainly higher in a growing market. In a market that’s about to be disrupted, defensive capital isn’t always the optimal strategy. Market factors are the most important variable affecting the decision to invest.

2. Casino-specific factors. Is the casino in a poor location relative to new competition? Is the property a market laggard? Can the casino be reimagined to capture unmet demand or steal share from competitors?

3. Where is the casino in its life cycle? Is it still enjoying high utilization and win per unit? Are its hotel rooms full? Is the property competitive? Is the physical plant/design up to date, and does it meet the needs and expectations of consumers?

4. Optionality. Does the decision to invest create more opportunities in the future? Can investment be staged? Are there valuable alternative uses for the property?

When considering these questions, a few examples might be instructive.

• Transformational investment. There are several examples of transformational investment in the gaming industry that have resulted in growth and renewal. These include the Hard Rock in Northern Indiana, where a declining riverboat complex was closed and the casino redeveloped at a nearby land-based location. The casino went from being the market laggard to the No. 1-performing casino in the market.

Hard Rock has implemented this strategy with similar results at several other locations, including in Iowa, Atlantic City and even at its flagship Florida property near Fort Lauderdale.

Hard Rock Northern Indiana, which originated as a riverboat, moved ashore and became the best performer in the market

The Atlantic City experience is particularly instructive. Hard Rock was able to take a failed property, purchase it at a steep discount and rebrand and reposition it, generating impressive returns. The conditions that allowed this were its lower entry costs, a stabilized market and an opening for a differentiated competitor in the marketplace.

The Florida experience is interesting because Hard Rock took a very strong performer and reimagined the project as an international destination, with outstanding results.

• Maturity-stage investments. Examples of casinos that have made successful mid-stage investments include the Oaklawn and Southland racinos in Arkansas. Both of these casinos had the good fortune of operating in a protected market without disruption and benefit from favorable legislation (table games) that paved the way for successful mid-stage development.

• Investing in a storm. We look to the casinos in both Connecticut and Atlantic City for examples of investment that resulted in larger balance sheets with limited results.

The Borgata in Atlantic City is also an interesting case. Atlantic City’s gaming revenue peaked in 2006 at $5.2 billion before an onslaught of new competition along the East Coast hollowed out the industry, eventually leading to a more than 50 percent decline in revenue and the closure of seven casinos.The Borgata opened in 2003 and quickly established itself as the market leader. By 2006, the property reported EBITDA of more than $250 million. The property opened with $1.1 billion of investment and, over the course of 20 years, invested a cumulative $2.2 billion in capital. Over that period, EBITDA declined by more than 40 percent between 2006 and 2013 before recovering back to around $200 million, but not anywhere near its peak.

Arguably, if Borgata hadn’t made those investments, it would not be near its current level of revenue or EBITDA—this is made clear by the performance of other casinos in Atlantic City.

A similar story played itself out in Connecticut at both Mohegan Sun and Foxwoods. The market forces that decimated Atlantic City had similar impact on eastern Connecticut. Both Mohegan Sun and Foxwoods have lower EBITDA today than in 2006, after more than $1 billion each in investment.

The lessons are clear. First, a strong balance sheet is required when investment is risky. Second, transformational investment works when a property is beyond its useful life and there’s no other choice but to start from scratch. This is the classic sunk-cost dilemma, where assets are written down and the investment equation starts anew. Third, maturity-stage investments make sense when the market still has the ability to grow, when new opportunities present themselves, and when the path to growth is clear. Fourth, investing in the storm is where it gets particularly dicey. At this point, we refer to the classic BCG investment matrix. It might be worth milking the cow instead of trying to keep an old dog alive.

However, if a market has stabilized and the new competition has been absorbed, that might be the time to dust off the old spreadsheets and invest in renewal.

Where Do We Go From Here?

For aging tribal casinos faced with new competition or for OPCO casinos in need of growth—do you milk the cow or invest? Sometimes there’s no choice but to keep an aging asset in place. In a market going through radical change, surgical and maintenance capital make the most sense. Maintaining competitive position while creating options for future development or diversification might be the best course of action. Waiting to invest might have value until the storm clears.

Maybe the mall example above can provide some insight. Successful mall development and renewal has been characterized by making a retail asset only one component of a larger mixed-use real estate development where residential, office, transit and entertainment facilities all come together to create a destination that feeds off itself. The gaming industry has tried this to some extent, always keeping the gaming component as the central strategic point.

Perhaps a wider approach is warranted. Live! Casino in Maryland is an excellent example (although the casino came after the other investment), as the property is one of the highest-grossing commercial casinos in the U.S. But it exists within a destination that includes many other components.

Live! Casino Maryland, one of the highest-grossing commercial casinos in the U.S., succeeds with the support of other components

Ultimately, there’s no universal prescription for extending a casino’s economic life. As properties move through maturity and toward decline, capital decisions must be grounded in a clear-eyed assessment of market dynamics, competitive positioning and optionality rather than reflexive reinvestment.

Transformational projects can unlock renewed growth when assets have outlived their original purpose and markets can support differentiation, while targeted mid-cycle investments can sustain performance in stable, growing environments. In contrast, deploying significant capital amid structural disruption often produces diminishing returns and balance sheet strain. For many operators, the most rational path may be disciplined maintenance paired with strategic patience—preserving cash flow today while retaining flexibility for reinvention tomorrow.

As with malls and other mature real estate assets, the future of gaming may lie not in doing more of the same, but in rethinking the role of the casino within a broader, mixed-use destination that creates relevance, resilience and long-term value. Cory Morowitz is managing partner of GGHM, a gaming industry advisory, analytics and investment firm.