The Philippine Casino Gaming Market

An exemplary case of competitive factors driving market recovery and growth in a post-Covid era

While the profound impacts of the Covid-19 pandemic continue to linger in many Asia Pacific gaming markets, the Philippine casino industry has been leading the region’s recovery and displaying signs of growth. The following examines how diversification and other key market advantages provides an exemplary case for post-Covid era gaming across Asia.

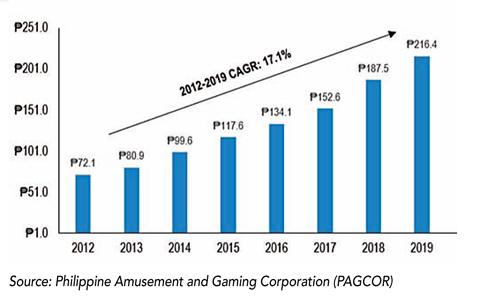

Land-based casino gaming in the Philippines was legalized in 1976. Since then, the industry has grown steadily over the past few decades (except during the pandemic-affected years) and has successfully secured its position among the top three gaming markets in Asia. From 2012 to 2019, the market’s gross gaming revenue (GGR) grew at a compound annual growth rate (CAGR) of more than 17 percent to achieve a record GGR of PHP 216.4 billion in 2019, more than three times the GGR in 2012.

Casino Gaming GGR in the Philippines (PHP in billions)

During 2020 and 2021, the market was severely impacted by protective measures instituted to curb the global pandemic, including closures, lockdowns, capacity limits and other restrictions. Nevertheless, the Philippine market’s GGR in the first half of 2022 has demonstrated a strong rebound with the recovery pace expected to accelerate—the 2022 total GGR estimate is anticipated to exceed the 2018 level and to reach nearly 90 percent of the 2019 level.

Solid Recovery Beginning in Q2 2022 (PHP in billions)

What is fueling the recovery and growth of the Philippine casino market? Our analysis indicates that the critical drivers include diversified product offerings, well-balanced market segments, expanding and enhanced capacity, an advantageous gaming tax regime, a solid workforce available at competitive costs, and the agglomeration of high-quality integrated resorts (IRs) in the country.

Diversification

The Entertainment City district in Metro Manila, the pride of the country, is a truly remarkable example of casino gaming and diversified leisure activities. Home to a number of prominent world-class resort complexes, the area provides a wide range of lodging, gaming, and other entertainment offerings. Moreover, Entertainment City arguably represents one of the world’s top IR clusters, along with the Las Vegas Strip and the Cotai Strip in Macau.

While these destinations have varying degrees of dependency on gambling, the agglomeration of casino facilities has undoubtedly shaped all three into top tourist destinations. The resulting “cluster effect” is expected to drive a strong and sustainable increase in future gaming and tourism demand.

The country’s anchor destination, Entertainment City, is complemented by other notable casino resort areas in Cebu and Clark. Cebu, a significant tourism destination and the second largest metropolitan area (after Metro Manila) in the Philippines, recently welcomed a new five-star IR, NUSTAR Resort and Casino, with Emerald Bay Resort and Casino expected to open next year.

The Clark Freeport Zone, a redevelopment of the former U.S. air base about 50 miles north of Metro Manila, is home to multiple high-quality gaming and hospitality properties. The upward dynamics in these markets unequivocally endorse the importance of diversification in terms of product offerings, source markets and beyond, which had been emphasized by many before the pandemic and have become even more critical in the post-Covid era.

Visitation

Fueled by solid local market segments and gradually increasing international visitation, the Philippine gaming market has been able to achieve substantial progress since early 2022. Within the current Asian gaming landscape, one of the most noticeable ongoing changes is the shift of junket-channeled VIP play to mass-oriented business. While it is true that mass gaming tends to yield a relatively higher profit margin than VIP business, it is important to not overlook the infrastructure and capacity required to handle the volume of mass visitation necessary to offset the decrease in premium business and achieve future growth. The Philippine market fills another exemplary role in this context.

Infrastructure improvements in the Philippines, ranging from enhanced connectivity between Manila and the neighboring regions to the newly added terminals at airports in Clark and Cebu, are expected to facilitate rapid recovery and further growth of the country’s gaming industry. The Clark International Airport’s new 10,000-square-meter terminal can accommodate approximately 8 million additional passengers per year. In addition to providing a more efficient gateway into Clark, it also is intended to ease air traffic congestion at Manila’s Ninoy Aquino International Airport.

Workforce

Further to above, one challenge that surfaced during the pandemic and continues to linger is the availability of a quality workforce. Shortages in skilled labor have hindered recovery and growth pace of economic activities around the world, and have been especially challenging for service industries like gaming. Mass gaming requires a larger workforce of quality, skill and reliability, which is likely to challenge many operators in the region’s gaming markets.

The Philippines possess another competitive advantage in this area. The local workforce tends to be comprised of fast learners who have the passion to work in most entertainment and hospitality settings. Meanwhile, labor costs in the Philippines remain among the most competitive in the ASEAN countries, attracting foreign investments and new operations to the country.

Taxation

Gaming tax rates and structure can have a significant impact on the potential success of an IR development and the acceptable return on private investment. Implementing a tax structure that attracts optimal capital investment while still deriving adequate revenue through taxes and providing ample funding for tourism promotion, regulatory oversight, and other associated social needs is critical.

The Philippines’ gaming tax regime remains commercially competitive in the Asia Pacific region, which represents a solid competitive advantage of the market, as operators can allocate more financial resources towards customer acquisition and/or capital improvements that result in greater prospective revenues.

While macroeconomic conditions and geopolitics between the Philippines and its key feeder markets may impose challenges in the years ahead, on balance, the Philippines gaming market is expected to grow in a sustainable manner thanks to its major business drivers and competitive advantages. The Philippine market already has set an exemplary case for the industry in the Asia Pacific region to evolve in a post-Covid era and will continue to build on that by capitalizing on the booming, and increasingly wealthy, middle class in the region, and better stimulating tourism and related economic impacts that benefit the country.