The Business of Gaming

Trends shaping the industry of today and tomorrow

Here at The Innovation Group, we are fortunate to see the gaming industry from all sides. With that perspective, we have had the honor of organizing and moderating G2E’s “Crystal Ball” sessions for the past several years, which ask key industry leaders to take a step back and reflect on where the industry is, and where it is going.

Our objective each year is to better understand how historical sectors (bricks and mortar, parimutuel, lottery) of the mainstream gaming industry are interacting among themselves, as well as with new and sometimes disruptive influences (HHR, sports betting, online gaming, media companies) to inform our audience and clients as they contemplate business development strategies.

Recently, the annual interval for this Crystal Ball dialogue has not been sufficient, as we find ourselves constantly reflecting on the industry’s evolution. Besides the swift pace of change, we are increasingly seeing forged relationships between legacy owner/operators and their incoming business threats.

The clearest recent example is the emergence of North American sports betting and online operations, which have made their way into the traditional gaming environment at breakneck speed. But we need not go back too far to recall when parimutuels became racinos and equipment manufacturers began running mini-casinos, which now compete with legacy casino operators all over the world.

In light of this fast-paced change, The Innovation Group has been adapting its approach to research and modeling, and in the process has identified several trends as we outline in the following.

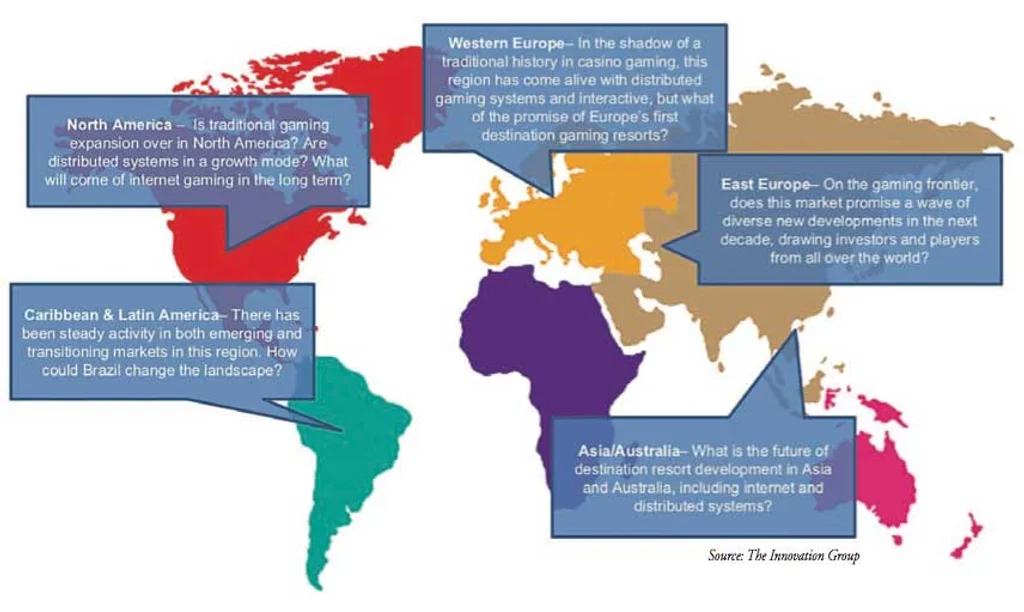

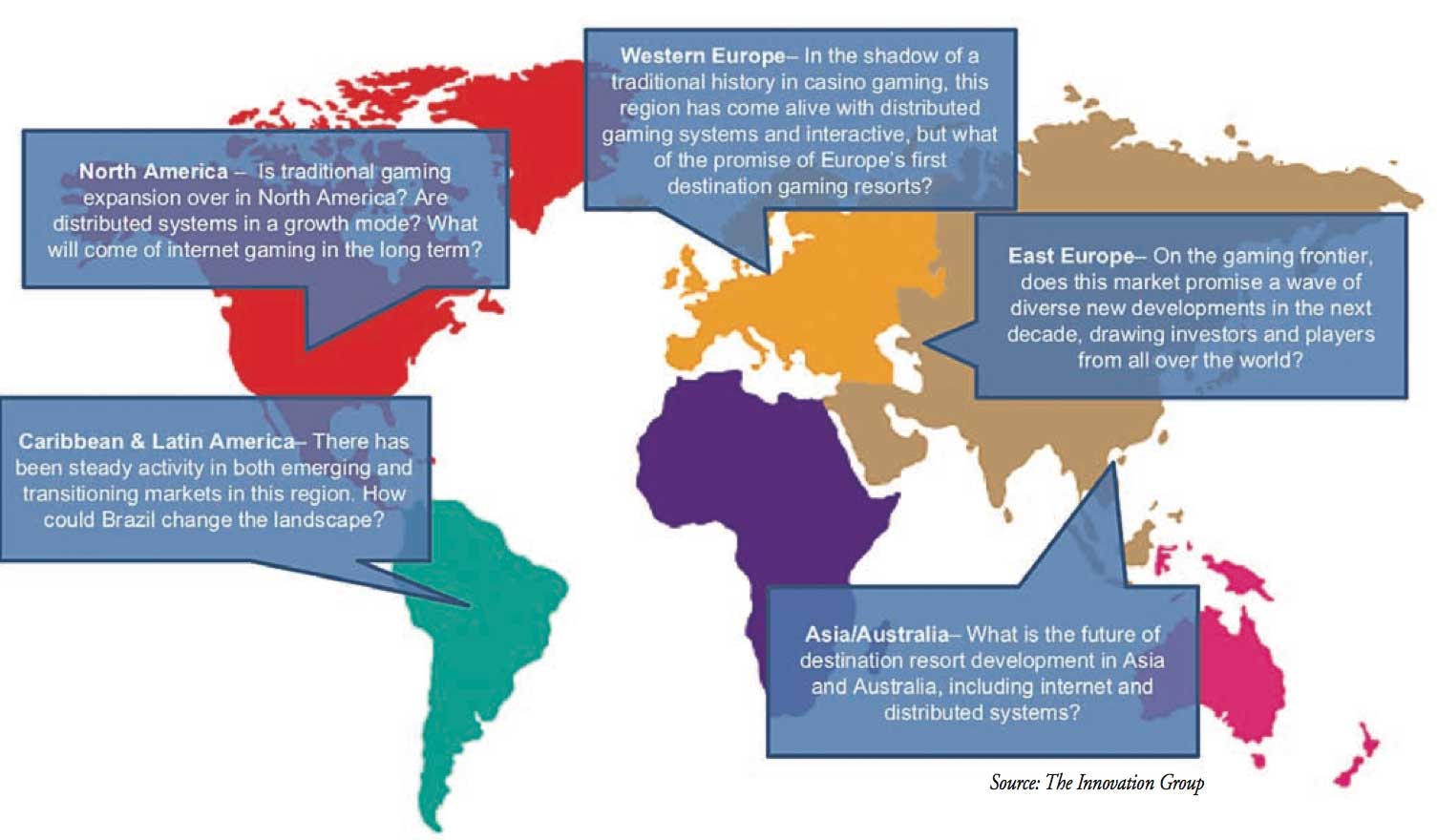

2016/2017: Industry Benchmarks

In 2016 and 2017, we held our first official conference sessions at G2E attempting to look at the gaming industry holistically. In the graphic, below, are some of the questions we were asking at that time.

And, here are how some of our expectations then materialized:

- Western Europe’s first IR was a much-anticipated development, which as yet arguably has not come to fruition.

- Eastern Europe was a wide-open market, but is more restrictive in gaming now than before and also in the grips of regional political turmoil.

- Japan’s effort to legalize casino gaming took some time off in 2016, but it was certainly in the background (where, practically speaking, it remains today).

- Australia was moving toward a meaningful expansion of casino licenses. Instead, outside of a few niche markets like Queensland and Sydney VIP, gaming in the region has been stagnant and weighed down by high-profile investigations into corruption as well as fallout M&A rescues.

- In Latin America and the Caribbean, we already were seeing wide casino and online expansion, which continues today, but all eyes were on Brazil IRs, which may still happen one day.

- In North America we spoke of the VLT movement, which has expanded in the U.S. and Canada, and added HHRs (historical horse racing machines) to the portfolio of distributed systems. We also were just then beginning to ask what would become of online gaming, which, despite massive expansion and the insertion of sports betting, is still a good question today.

The Past Five Years: What’s Hot and What’s Not

The Innovation Group’s Crystal Ball perspective for each year since 2016 is organized roughly into pre- and post-Covid periods in the chart on the following page. In a real sense, it was only during Covid that many of us acknowledged that change in the gaming industry—like other businesses reliant on leisure technology platforms—was ramping up dramatically. Interest in topics like data science, blockchain, online gaming platforms and payments emerged at later stages in the industry’s trajectory, but with a much more concentrated business development focus. Increasingly, these technology-driven business development categories seem more likely to be absorbed into gaming horizontally, in contrast to the vertical integration that brought casinos, parimutuel facilities and route operations together.

The graphic, below, reflects our sense of “what’s hot and what’s not” historically, and going into 2023. There are fine lines around some of the product categories as outlined, but for a qualitative review the distinctions should work. You can observe that 1) the darker the demarcation of the input, the hotter the topic; and 2) the closer together the hot topics, the more quickly and intensively they have been explored.

2023: Short-Term Trends

We are so used to discussing the unique forms of gaming critically, the simplicity of the manner in which trend information is illustrated in the chart can be misleading—the less-obvious cultural and long-term influences on the industry lie below the surface. Our holistic interpretation of these observations takes a few forms, which we share below.

Schism Culture. The speed of change in gaming and its technological nature have created a wide knowledge gap between its seasoned executives and emerging leaders. Within the companies developing gaming technologies, this trend is likely no more disruptive than in any other technology-dependent industry. But in operating companies, this is manifested in routine planning meetings where seasoned decision-makers have to rely heavily on input from professional peers who speak an almost entirely different language. For example, within gaming operations that are in transition, where competing player engagement strategies spar for resources, it seems that neither traditional nor new data-driven forms of marketing have really nailed it across the many types of players in the mix.

Dilution of Control. One of the most consequential advantages of the gaming industry is also one of its greatest weaknesses: We are insular. For example, it took traditional gaming companies several years to truly accept the earliest forms of loyalty and CRM—perhaps a decade behind airlines and credit cards. So, as the industry got its marketing analytics, operating platform technologies and security protocols together, the DNA of the tech companies helping make those technological transitions adopted the industry itself. We see this in the online space, in payments, and even security technology companies that have entered the lottery and platform technology (CMS) development businesses. The result is a dramatically diverse makeup of businesses that today identify as “gaming companies” and, thus, a dilution of industry control previously held by its operators.

Reorganization Fatigue. Gaming, lodging and leisure as a broader industry has been deconstructed and reconstructed many times, mainly for the purpose of boosting company valuation multiples. This trend began with the disaggregation of gaming and hotel assets into separate companies in the late 1990s. Following the Great Recession of 2008, private equity rescued publicly traded gaming companies, only for those companies to return to being publicly traded businesses again by 2015. Since then, gaming companies have been bisected again, this time into operating companies and real estate holding companies.

It should be noted that over the same period Indian tribes and First Nations have maintained the most competitive, private (sovereign) gaming operations.

Even with all these changes, until the emergence of the global pandemic in 2020, the core of the industry has always seemed whole. With the exception of gaming equipment manufacturers and a limited number of online gaming and sports betting companies (which can benefit from having neutral relationships with operators), everything has been absorbed. A diversified owner-operator in gaming today operates casinos, racinos, online gaming/sports betting, and in many cases distributed systems (VLTs or HHRs).

However, since the pandemic, the ability for these diversified companies to compete is more and more reliant on incongruent relationships. For example, do we expect casino companies to own sports teams, media companies to own casino companies, or vice versa? And is all of this just for an edge in marketing or ultimately for control of data and customer relationships? Only time will tell.

Issues Amplification: Responsible Gaming and Illegal Gambling. A more nuanced and recent development in gaming is a renewed interest in responsible gaming (RG), particularly by regulators who seem to be responding to public sentiment (if not scientifically founded) that expanded forms of gaming will increase risk. The industry has been both responsive and proactive, taking the opportunity to reevaluate advertising practices and address the confusing problem gambling helpline structure in the U.S. Simultaneously and congruently, a concerted effort is under way to combat illegal gaming institutions in all their forms (slot and VGT arcades, online and sports betting operations) that cut into legitimate gaming company profits and offer no remediation measures to address problem gaming. For our part, The Innovation Group is engaged with the International Center for Responsible Gaming and assisted the American Gaming Association in its research on illegal gaming practices.

Crystal Ball Redux: How to Stay Ahead of the Curve

Six months out from our last review, and six months ahead of our next Crystal Ball discussion, our key finding here is simple: It is more difficult than ever to stay ahead of the gaming business development curve. Trends like blockchain, AI and the metaverse will have a shorter conceptual life within gaming before becoming mainstream applications. It is the behaviors that respond to this more difficult business development environment that will define the future shape and success of gaming.

Of course, our industry is not unique. Most industries are dependent upon adapting to changing technologies and structural realignments. So, what can we do to adapt more effectively to the accelerated pace of change? Here are two big ideas for your consideration:

Hyper-embracement of the next generation of gaming professionals. There are several programs—The Innovation Group’s Emerging Leaders of Gaming (supported by this publication), Global Gaming Women and African Americans in Gaming, among others—bringing brilliant young gaming professionals together to share new ideas. These ideas are more valuable than ever in the C-Suite, as senior managers in gaming are younger on average every year. Clearing out some space at the top of the hierarchy in operating companies sooner than later should bode well for more progressive competitors.

Revisit how strategic planning is conducted. The quintessential five-year strategic plan is dead. Maybe even the three-year plan is too short. We should be treating strategic planning dynamically, the same way we adapt operating forecasts over the course of a year. Then we will be better prepared to capitalize on opportunities and not be so surprised that the plan on the shelf was not a good indicator of what is happening today.

As we consider the next decade of gaming, The Innovation Group is optimistic for the industry’s future value however it is shaped and sized. Most jurisdictions have moved well beyond the stigmas in gaming’s past and are looking for ways to generate more and more fiscal revenue through its entertainment-driven experiences. We look forward to the eminent discussions at this year’s Crystal Ball session that will further chart the path forward.