10 Trends for 2022

As the industry continues to recover from the Covid-19 pandemic, leaders look forward to new revenue streams

With the December issue of GGB, as always, we look ahead to the major trends the industry is likely to experience in the coming year. Last year, of course, was different than any previous year, thanks to the Covid-19 pandemic and subsequent industry shutdowns.

The pandemic continues to cast a shadow over any future predictions for the gaming industry, as many jurisdictions around the world continue to struggle to recover visitation and travel restrictions remain in place.

Two of the trends we analyze in the coming pages are particularly reliant on those restrictions easing. The Chinese government continues to strictly regulate visitation to Macau, which is likely to struggle for some time before regaining its status as the world’s leading gaming jurisdiction. In Japan, the continuing pandemic keeps bumping back the time when planned integrated resorts will launch, and which operators will end up building them.

Another major effect of the pandemic has been a shortage of qualified workers, many having failed to return to their jobs as casinos reopened.

Meanwhile, many positive trends can trace their momentum to the pandemic shutdowns—particularly sports betting, iGaming and the move toward cashless gaming across many worldwide gaming jurisdictions. We include an examination of how the rapid expansion of sports betting could potentially trigger a backlash if responsible gaming measures are not secured. And in cashless gaming, the regulatory community is key, as operators work toward offering patrons cashless options.

Other bright spots for the coming year include esports, which continues a meteoric rise in popularity and in betting opportunities; distributed gaming, which has been a stable sector consistently and could be poised to grow in many states; and the recovery of the U.S. casino industry to levels exceeding pre-pandemic business.

The past two years have seen unprecedented challenges for the casino industry. Here, in our view, are the key factors in meeting not only those challenges, but new opportunities.

1. Beating the Pandemic

It’s been a long nightmare shared by the world. Covid-19 impacted every corner of the world, but industries that depended upon people traveling, attending or participating were hit hard. The casino industry experienced unprecedented circumstances that included shutdowns, gaming floor redesigns and operational changes that will long survive the pandemic as it winds down.

It’s been a long nightmare shared by the world. Covid-19 impacted every corner of the world, but industries that depended upon people traveling, attending or participating were hit hard. The casino industry experienced unprecedented circumstances that included shutdowns, gaming floor redesigns and operational changes that will long survive the pandemic as it winds down.

The recovery has been spotty around the world.

In Asia, the impact continues. Casinos in Australia only recently reopened after at least 18 months shuttered. In New Zealand, casinos opened and closed several times, as even one case of Covid caused the government to reinstate draconian lockdowns.

In the Philippines, capacity limits were only lifted last month to more than 50 percent, and development of new casinos in Cebu and possibly Boracay remained on hold.

Cambodia was one of the early success stories during Covid. Authorities closed the borders and avoided the spread of the disease by instituting a “watertight” quarantine-on-arrival system. But even that system broke down, and casinos became the epicenter of Covid spread earlier this year, particularly in Sihanoukville.

Macau casinos reopened after closing for a month in early 2020. But the impact of the pandemic lingers to this day as the governments of China and Hong Kong continue to strictly control border crossings. Quarantines were necessary until just recently, and new Covid cases caused Macau authorities to twice implement testing for every resident and visitor to the SAR. Macau revenues have plummeted and still are on life support. And all this is playing out as the Macau government considers how the concession renewal process will proceed.

European casinos were of course heavily impacted, but the degree was different in each country. The United Kingdom opted for almost a year of closures, while in a country like Sweden, which imposed few restrictions on its citizens, casinos remained open unless a Covid breakout was present. Today, most European casinos have reopened, but restrictions remain, depending upon the country.

Canada was a country that locked down its borders and imposed strict controls on travel and access to businesses. While each province was different, most Canadian casinos remained closed until just recently, as the borders reopened only to fully vaccinated travelers.

In the U.S., “two weeks to stop the spread” became at least three months. Leading the way when casinos reopened was tribal gaming. In many cases, tribal gaming is the only revenue stream for tribal governments, so reopening safely was essential. They became the model for the reopening of commercial casinos across the country, including Plexiglas barriers, widespread sanitation, and social distancing on the casino floor.

And once the casinos did reopen even with capacity restrictions, revenues came roaring back. U.S. casinos have now equaled their 2020 revenue numbers in the first three quarters of 2021.

The silver lining of the pandemic was the increased revenue of online casinos in jurisdictions where they are legal. In New Jersey, online revenue doubled and tripled during the lockdown, and once the Atlantic City casinos reopened, online revenues continued to climb. Sports betting was legalized in many states as well during this period, and revenue records were set month after month. Today, many states are now considering legalizing online gaming to avoid losing the entire gaming tax base, should another pandemic arise.

—Patrick Roberts

2. Esports and Esports Betting Surge in the U.S.

Esports are a type of sport where electronic systems facilitate the primary aspects of the sport. Both the input and output of the esports system as well as that of the players and teams are mediated through human-computer interfaces. Esports are competitive video gaming, both amateur and professional. They are often organized by multiple leagues, ladders, and tournaments. Players usually belong to teams or other organizations that sponsor them.

Esports are a type of sport where electronic systems facilitate the primary aspects of the sport. Both the input and output of the esports system as well as that of the players and teams are mediated through human-computer interfaces. Esports are competitive video gaming, both amateur and professional. They are often organized by multiple leagues, ladders, and tournaments. Players usually belong to teams or other organizations that sponsor them.

Esports has been one of the fastest-growing forms of media in recent years due to the increasing popularity of online games and broadcasting technologies. In 2021, esports were watched by more than 474 million people. Six years ago, that number was only 70 million. The figures in the U.S. are also increasing exponentially. This is attracting major interest from esports-centric end-to-end betting solutions such as Oddin.gg.

Venture capitalists and, more recently, private equity firms have invested significantly in the industry. Esports teams are just like professional sports. They have owners, franchises and endorsement deals. Cash prizes can also be won from tournament wins. Their total revenue and valuation are affected by all of this. Forbes reported that TSM was the most valuable organization in esports, valued at $410 million as of 2020. Cloud9 is second at $350 million, while Team Liquid comes in at $310 million.

Esports leagues are likely to resume their efforts at expanding their audience by hosting live game play with regional teams in an esports format that is more similar to traditional sports leagues. According to most projections, the esports industry will surpass $1 billion in annual revenue this year. NewZoo predicts that revenue will grow to $1.8 billion by 2022.

Mobile will be the future of esports. This will reduce entry barriers and allow more fans and gamers to play. Mobile gaming will account for 45 percent of all global games sales this year. This popularity is already affecting some competition spaces with the creation of new leagues in the U.S. at high schools, colleges and cities across the country.

Live streaming is a key factor in the rise of esports. Esports reached a turning point in 2010 when access to broadcast technology at the consumer level and platforms like Justin.tv (later Twitch) allowed events of all sizes and scope to grow beyond their regional boundaries. The thrill of these experiences attracted a larger audience, and soon concurrent viewers of broadcasts became the measure of success.

Because streaming is an intrinsic part of the esports ecosystem, developers need to think about the possible impact of esports when creating competitive games. Esports games must be entertaining for both players and viewers. A game must be simple enough for all levels of competitors to stream in order to maximize its reach.

Global Web Index research shows that 53 percent of Gen Zers (defined as people born between the mid-1990s and the early 2010s) identify themselves as sports fans. This compares to 63 percent of all adults and 69 percent of millennials. Gen Zers are twice as likely as millennials not to watch live sports and half as likely to do so regularly than they are to never. This is partly due to their attention to esports. Gen Z is more interested in esports than MLB, NASCAR, and the NHL, with 35 percent of them identifying themselves as fans.

Explains Becky Harris, former chair of the Nevada Gaming Control Board and an adviser to Oddin.gg, “As the popularity of esports continues its meteoric rise, continues to become more integrated in cultures around the world, and regulated sportsbook operators continue to explore ways to incorporate wagering on competitive play into their wagering options, more contemplation and consideration needs to be given to the potential of esports.”

The relationship between the world of esports and sports betting is getting closer, and this is due to the professionalism of the former. If a few years ago video game sports were reserved only at a social level, now there are more and more professionals who live from this. The championships have gone from a regional area to being of a global nature, while the prizes have already accounted for millions of dollars.

This growing interest in esports has also attracted the attention of the sports betting sector. The houses already see the esports modalities as safe and reliable to offer games in their market. If there are millions of fans who follow it on the internet and they are absolutely professionalized championships, there is no reason to avoid this offer in sports betting. Users can make their forecasts, both before each game or during the course of it. In fact, live betting is the most popular, as it generates double excitement and tests the capabilities of players.

Nevada, New Jersey and Tennessee are the only states that completely allow esports betting. Esports betting is also regulated in certain states. This means that there are restrictions and rules, but it is not illegal. Esports betting in the states of Arkansas, Delaware, New York, Iowa, Illinois, Michigan, Rhode Island, Montana, New Mexico, Oregon and Pennsylvania is legal and regulated.

This all leads to the conclusion that esports will continue to be an integral part of the sporting scene for many decades. This implies that esports betting would be accepted by a large segment of the population, much in the same way as traditional sports betting.

The U.S. has a long history of sporting excellence. NFL and NBA data and interest show that there is a huge market that could be open to esports alongside traditional sports. Many U.S.-facing betting sites already offer local bettors a mixture of esports and classic sports betting. This means that esports betting in the U.S. could be a major global phenomenon.

The U.S. has more than 160 million gamers and is, therefore, the second-largest gaming market. American publishers and developers of games like Riot Games and Epic Games have helped to create some of the most prominent players in competitive gaming. In addition, esports betting sites in the U.S. have started to capitalize on the growing popularity of esports betting and cover all important tournaments and games.

Although the foundation is in place, there are still many untapped opportunities.

—Marek Suchar is CEO of Oddin.gg, a company dedicated to streamlining esports betting

3. Stability in the Routes

The distributed gaming sector traditionally has been one of the most stable in gaming. Machine routes in eight states have produced reliable returns over the years for what is a relatively small group of route operators.

Of course, like every other sector of the industry, distributed gaming was disrupted by the Covid-19 pandemic. In fact, the routes were disrupted more than the traditional casinos in the largest distributed market, Nevada. While slots in casinos were idle around three months, route operations in bars were shut back down, and remained idle until October.

“The state of Nevada enacted a rule that no one could sit at a bar, or play a game at a bar,” says Blake Sartini II, senior vice president of distributed gaming for Golden Entertainment, one of the largest distributed operators in the nation with more than 11,000 machines on routes in Nevada and Montana. “With 70 percent-80 percent of our distributed games located in bars in Nevada, that definitely hurt.”

Sartini says the operators didn’t encounter the same problem in Montana, which was back up and running by May 2020, and since Nevada reopened, business rebounded, and has even experienced organic growth—a combined effect of population growth in Nevada and an influx of current slot players who were nervous to return to crowded locals casinos.

“Southern Nevada is seeing a record number of California residents move into town, and we are seeing a significant number of those people show up at our taverns and sign up for our rewards card,” Sartini says. “In distributed gaming, we are the great outlet for anyone moving into the state.” He adds that the operator also saw organic growth in Montana, where the route market has remained stable.

Illinois has been another stable market for distributed gaming, although the competitive balance changed this year when Accel Entertainment, the largest route operator in the state, was acquired by Century Gaming, Inc., Golden’s closest competitor in Nevada and Montana. Century operates around 8,500 machines in Nevada and Montana and has added more than 12,247 machines Accel operates in Illinois—around a third of that market.

Sartini says Golden maintains a license in Illinois, and is always open to opportunities to establish a footprint there.

“We consistently look at opportunities in that state,” he says. “We have a license at the ready and available to use if and when we find the right opportunity.”

While all the route operators should see sustained growth in existing markets next year, all are heavily involved in lobbying efforts to expand the market beyond the current routes in Nevada, Montana, Illinois, Oregon, South Dakota, West Virginia and Pennsylvania—the latter a very small market consisting of six-machine operations at truck stops.

Sartini says the best opportunities for new distributed operations within the coming year are in Pennsylvania, where bar and tavern owners have long pushed for VGTs; and Missouri, where there have been VGT bills active in every legislative session for several years.

“We have been working in Pennsylvania for five years, and Missouri’s got a game plan,” Sartini says. “We’re hoping to at least get a bill through committee in the upcoming session, and hopefully get it to the floor for a vote.”

He adds that there is continued discussion on VGT bills in Virginia, North Carolina and other states, where the route operators maintain lobbying efforts.

In addition to educating lawmakers on the benefits of distributed gaming, those lobbyists in many cases are working against the interests of companies that have placed unregulated “skill games” in those states. While Virginia instituted a ban on the unlicensed games effective July 1, Wyoming passed a bill legalizing them. In Pennsylvania, casinos and lobbyists continue to wage a battle to eliminate more than 20,000 of the skill games spread across the state.

There has been some backlash to skill-game bans from small businesses that benefit from the revenue those unregulated games generate, but Sartini says that backlash should provide an opportunity for legitimate distributed gaming.

“While we’re working against the illegal skill game operators, these small businesses need some help amid all the turmoil they’ve been through, and VGTs/distributed gaming can solve that—just in a regulated manner,” he says.

Meanwhile, the established distributed gaming markets will keep chugging along. “We are always focused on expansion and growth in other markets, but we have a very successful existing business right now,” Sartini says. “It has gained a lot of momentum over the last 12 months, and we feel we can use that momentum and the operational nuances we have put in place to help us be in a better position in 2022.”

—Frank Legato

4. Asian Recovery or More of the Same?

Heading into 2020, it looked as though the gaming world would continue on its track of expansion in Asia. Macau was two years out from concession renewal. The Philippines was seeing strong growth in gaming and tourism. Jurisdictions such as Cambodia, Vietnam and others were seeing strong growth in their existing facilities with new projects being announced along the way.

Heading into 2020, it looked as though the gaming world would continue on its track of expansion in Asia. Macau was two years out from concession renewal. The Philippines was seeing strong growth in gaming and tourism. Jurisdictions such as Cambodia, Vietnam and others were seeing strong growth in their existing facilities with new projects being announced along the way.

Yet, it was shortly after the start of that year that the world began to change, and change rapidly. Macau initially shut down for two weeks, and the rest of the world soon followed with what still remains for many jurisdictions that are in Great Shutdown mode. Gaming revenue evaporated quickly. Timelines for expansion disintegrated. Concession renewals in Macau were put in limbo other than a two-year extension to put all of the concessionaires on the same timeline for renewals. Heading into 2022, there are just as many uncertainties as portions of Asia finally began to reemerge from nearly two years of lockdown.

One of the overarching issues as one looks at the Asian market with a focus on southeast Asia, and specially Macau, is understanding these markets are fueled by the flow of visitors in and out of China. The country still believes in a zero-Covid policy, which has kept the flow of visitors from Guangdong exceptionally slow at times and limited visitation to nearby Macau. A disappointing Golden Week along with Macau implementing mandatory testing for a period of time did not bode well for the last quarter of 2021, and news that the Hong Kong border would be open “by June” as stated in November is less than optimistic as the world’s largest gaming market tries to regain its prowess.

There are two other hindrances to an early recovery that stem at the root of Beijing’s control over the flow of Chinese tourists in and out of the country. The first of these is the hosting of the 2022 Winter Olympics in Beijing in February. China wants to make sure this goes off without a hitch, and that will include making sure that the number of Covid-19 cases does not flare up. The only way that happens is if they keep the country in lockdown mode.

The second is China’s policy toward gaming in general and the mysterious “blacklist.” President Xi Jinping clearly believes that gaming breaks up the “social harmony” of China. He has used the pandemic as a tool to further solidly this position with a supposed backlist that would ban Chinese visitors from certain jurisdictions that the PRC finds to be exploiting visitors by luring them to participate in gaming.

While it is still unknown who is on this list, the reach is far and has wide implications—from preventing citizens from visiting certain areas to the recent arrest of over 140 individuals that were illegally marketing for Tigre de Cristal in Vladivostok.

The challenges for Southeast Asia, and any other jurisdiction that relies heavily on Chinese tourists, is not only when they may return, but if they will be allowed to return at all. Some of these outposts will continue to have some traffic because of settlements of Chinese nationals in these countries to support the Belt and Road Initiative.

However, some of these jurisdictions may not see the return and, in some cases, might not be able to use the same tactics with junkets to allow customers and gaming dollars to flow in and out of the country. With all of these challenges on the horizon, gaming will start to materially recover closer to the second half of 2022 as the world reopens. Granted, one new variant of the virus could cause another shutdown, but countries and individuals are realizing that the world cannot shut down forever.

As 2021 closed out, the gaming industry started to reopen in key Southeast Asia markets as capacity constraints and borders have started to reopen. This will bode well for markets including Cambodia, Vietnam and the Philippines that have struggled through most of the last two years. It likely means that these markets will continue to rebound and likely start to see some of the expansion that was sought after two years ago, before the pandemic began.

The biggest item that will bring some clarity through 2022 is the concession renewals for Macau. While there are still many questions that need to be answered, renewals for all operators seem more likely than they did when the process was initially launched in the fall of 2021. However, the conditions and process to achieve these renewals may make it difficult for the market to return to its previously held records.

The challenge will be to find a path forward that allows operators that have invested billions of dollars into a market to continue to operate in a manner that benefits all parties. As the world watches what will happen in the largest gaming market in 2022, significant opportunity lies across all of Asia along with the potential risks that remain for the industry should parameters change.

—Brendan D. Bussmann is a partner and director of government affairs with Global Market Advisors (GMA)

5. For the Love of the Game

Sports betting has dominated the gaming industry’s attention over the last several years, and its emergence with the repeal of the Professional and Amateur Sports Protection Act in 2018 became a particular bright spot in 2020 as casinos were impacted by Covid-related closures and capacity constraints. Indeed, even while major worldwide sports were sidelined, we saw heavy wagering volumes (and increased online viewership) in Japanese sumo wrestling and Russian table tennis. The sports betting boon has bolstered not only gaming company financials but those of teams and leagues.

Sports betting has dominated the gaming industry’s attention over the last several years, and its emergence with the repeal of the Professional and Amateur Sports Protection Act in 2018 became a particular bright spot in 2020 as casinos were impacted by Covid-related closures and capacity constraints. Indeed, even while major worldwide sports were sidelined, we saw heavy wagering volumes (and increased online viewership) in Japanese sumo wrestling and Russian table tennis. The sports betting boon has bolstered not only gaming company financials but those of teams and leagues.

Once among the fiercest opponents of sports betting, teams and leagues have developed a newfound love for the industry and the opportunities that sports betting provides for further monetizing their product. Mark Cuban remarked upon the repeal of PASPA that the value of all sports franchises doubled overnight, and in the more than three years since, we have seen partnerships between teams and sportsbooks, leagues and sportsbooks, and combinations that can even include media giants such as NBC, CBS, ESPN, Sinclair and others.

The nuance of these deals can be incredibly complex, but the concepts driving them are incredibly simple. Teams, and leagues by extension, are in the business of delivering content to fans. They monetize the content in three main ways: direct sales and sponsorships at the stadium or arena; digital viewership, primarily on television, which stations monetize through advertisements; and brand and merchandise. Several studies have linked sports wagering to increased propensity for game viewership and increased duration. In other words, when you’ve got a bet on the game, you are more likely to watch and watch until the end. Increased viewership translates to increased value of the ads, which in turn means that teams can charge more for the broadcast rights.

Teams also command seven-figure sponsorship deals from sports betting operators that are creeping toward eight figures for exclusivity in some markets. Notably, these partnerships are not only for the biggest of leagues. The Premier Lacrosse League announced a deal with DraftKings, the LPGA cut a deal with BetMGM, and PointsBet signed a deal with the Colorado Buffaloes, a college team. Besides any cash infusion the team or league might receive, a partner sportsbook focusing on a menu of betting options specific to the team or league has the capacity to increase interest in and viewership of games, which has tangible benefits in all of the team or league’s monetization efforts.

Meanwhile, the sports betting operator benefits greatly from these deals as well. Most pressingly, the operators are paying for physical and digital signage at the stadium or arena, resulting in high-quality ad impressions from fans—after all, who is more likely to bet on a sporting event than someone who paid to go to the game? Caesars even recently purchased the naming rights for the Superdome in New Orleans, a first-of-its-kind deal in the U.S., reminding fans and even daily commuters who see the stadium signage to place their wagers at Caesars Sportsbook.

Generally, sponsorships often also include (limited) use of the team’s intellectual property, such as logos and other creative, providing the operator a boost in credibility as they push ad campaigns through social or traditional media channels. The operator also gets unprecedented access to the team, which may include such allowances as arrangements for casino VIPs, celebrity appearances at parties hosted by retail sportsbooks, or even potentially unique mobile betting menu options authorized only within the stadium or arena.

Despite all of this, only very recently have teams and leagues taken the final integrative step—actively offering betting themselves or at the arena. Besides sports betting revenue, in-arena venues typically have access to food and beverage availability and merchandise, and they are open for business even on non-game days, again expanding the team’s ability to generate revenue. William Hill opened the first in-venue sportsbook at Capital One Arena in Washington, D.C., and since then Rivers has followed suit in Pittsburgh’s PPG Paints Arena, among others that have been announced.

Arizona took this a step further in 2021, when legislation passed that allotted 20 sports betting licenses in total, 10 reserved for tribes and 10 reserved specifically for professional teams and leagues. The Phoenix Mercury (WNBA), the Phoenix Raceway, the Arizona Cardinals, the Arizona Diamondbacks, the Phoenix Suns, TPC Scottsdale, and the Arizona Rattlers (indoor football) have all announced sports betting partners, and many offer or plan to offer betting on-site. Sports team partnerships were called out specifically in the New York sports betting license applications, and we can expect to see these partnerships expand in scope over time.

Looking ahead to 2022 and beyond, particularly with the team-friendly result achieved in Arizona, expect to see teams actively engaged in the pre-legislative process, wielding their considerable resources and leverage with politicians to effect policy decisions favorable to their interests, whether they are looking for licensure or simply the ability to offer sports wagering in a co-branded lounge within the venue.

The teams’ and leagues’ considerable political influence and fiscal wherewithal, coupled with their existing partnerships with both casinos and media companies, can make them either a critical ally or a formidable foe in adopting legislation that balances the diverse viewpoints of casinos, sports betting operators, and other relevant entities.

—Brian Wyman is a partner at The Innovation Group

6. Fixing the Regulations

“Chaos is a friend of mine.” —Bob Dylan

The first significant attempt to regulate gambling in modern times was undertaken by Nevada in the mid 1950s and intensified in the early-to-middle 1960s. It was done, arguably, to protect the industry from itself.

Accusations concerning inappropriate conduct, primarily by the suggested presence of organized crime members, had made Nevada’s gaming industry the target of the federal government, and there were concerns in the state that this drama would not end well. The response was to build a regulatory agency to act as a moat for the industry in its drive toward legitimacy.

By and large, the Nevada regulatory model developed in response to this threat worked. Not only did this system allow gaming to be sustainable in Nevada, but it created a brand that proved suitable to export to many of the states of the United States in the decades that followed.

Over the last few years, the gaming industry in the U.S. has undergone the shock of adapting to a new delivery system for gaming products—namely, the use of the internet. This has been primarily evidenced by a rapid legalization of mobile sports betting in many states and with a lessor adoption of iGaming.

As mentioned, the most threatening problem the gaming industry had initially in Nevada was with organized crime. In today’s regulatory environment, we seem to be embracing something that is not necessarily crime, but it is certainly very unorganized.

If there is a trend to all of what is going on in the United States with respect to the regulation of gaming, it is that the regulators are overwhelmed. The agencies are understaffed and underqualified to handle much of what is taking place. Moreover, the politicians are not helping.

In state after state, the launch date of sports betting is set to meet the demands of the sporting calendar, such as to be open by March Madness or the start of the NFL season. These launch dates should be established by one measure, and that is when the regulatory infrastructure is in place and the regulators are ready.

Essentially one-third of the states that have expanded gaming through internet products have done so without addressing the issue of potential gambling harm to consumers. Issues that have plagued places like Tennessee, Washington, D.C., Oregon, and the efforts evolving in New York (to mention just a few) certainly will not be listed in any “best in category” awards, at least in the near future.

One obvious problem with the regulatory entities is that the staffs of these organizations have very weak benches, or no bench at all, as to understanding the complexity of sports betting. This is easily understood, for in most states the regulators have no experience in regulating sports betting. Moreover, most agencies are staffed by brick-and-mortar regulators who do not necessarily understand all of the many details and nuances of delivering gaming products in a virtual world.

Countering the notion that what you don’t know can’t hurt you, there is a tremendous gap in the understanding of the importance and operation of artificial intelligence in shaping the interactions between the betting operators and the consuming public in this new world of betting in the U.S.

In addition, especially in the higher levels of many of our agencies, there is not much depth in data analytics, and in the virtual world, this is a knowledge and skill that touches on the entire marketing ecosystem as well as on the ability to detect fraud, money laundering, and problem gambling (to mention just three). It is also the case that the leadership in many of our agencies do not possess the necessary backgrounds and skill sets necessary to understand the reality of what they are now expected to regulate.

If all of this isn’t enough of a challenge, it seems there are now concerns that address advertising. I live in Pennsylvania, and have noted as I was watching a series of gaming advertisements that this sequence was briefly interrupted by the news. There has been some use of the bully pulpit by people in authority to address this issue, but if one understands game theory, this certainly will not work. And if we believe it is an appropriate role of the government to tell a business how often it can communicate with a market, we are entering into a whole new world of slippery slopes for the bureaucrats.

The point is the major trend in regulation right now is it is overwhelmed. It needs more and better assets, and this takes time and money. It also takes patience. I believe this goal could be obtained if we had a bit more adult supervision, and unfortunately this seems in short supply in the modern world of gaming.

A few steps in the right direction would be to be less concerned about the apparent needs of the operators to achieve immediate world domination. We need to keep politicians away from our gaming agencies and allow them to feather their government pensions somewhere else.

Regulatory agencies are not rest homes for termed-out politicians or those who lost an election. We need to pay our regulators real money, and we need to recruit talent that possesses the skill sets that are relevant to the industry that we have today.

In short, we need to become alive to the necessity of building our regulatory agencies for the industry we have, not the industry we had.

—Richard Schuetz is a former casino executive, regulator and educator, expert in all things gaming

7. Go Big or Go Home

The biggest trend in responsible gambling for 2022 will be nationalization. Historically, each state government and regulatory agency set their own responsible gambling requirements, with little if any coordination between other states or even among different verticals within the state.

The biggest trend in responsible gambling for 2022 will be nationalization. Historically, each state government and regulatory agency set their own responsible gambling requirements, with little if any coordination between other states or even among different verticals within the state.

Most gambling operators also traditionally viewed consumer protection from a state-based perspective. This has led to our current patchwork of responsible gambling regulations, which has long been difficult to navigate for consumers.

This state-by-state approach to responsible gambling in national broadcast, worldwide streaming and global social media increases costs and creates barriers to help. However, the rapid expansion of sports betting across the country, the largest and fastest in our history, will also lead to the nationalization of responsible gambling programs.

The blitz of sports betting advertising during league broadcasts requires a national responsible gambling approach. Many states specify the use of their own state-specific help line numbers which were created decades ago. So gambling ads have to list dozens of state helplines to be in compliance. Callers who may be in crisis have to pick the right number out of dozens (in tiny font on screen for mere seconds) or they end up at the wrong state help line.

Fortunately, the National Council on Problem Gambling’s National Helpline number instantly and automatically connects callers to the help line call center in their state—just as 911 instantly and automatically connects callers to their local police emergency line. A number of regulators have recently adopted rules allowing operators to use the National Helpline number on ads in their states, but more than 20 states retain their antiquated requirements.

Many other responsible gambling services are ripe for a national approach. Consumers who have a gambling addiction and want to self-exclude have to sign up with hundreds of different programs, in many cases traveling to the casino or sportsbook to sign up in person to exclude themselves from that very location.

This may actually increase the risk of relapse. Advocates are working to create national-level consumer-centric approaches to responsible gambling that will increase accessibility, improve compliance, raise awareness, boost efficiency and decrease barriers to life-saving services for people at risk for gambling problems and their families.

—Keith Whyte is executive director of the National Council on Problem Gambling

8. Japan Crosses The First Finish Line

With the Olympics being a made-for-TV event, Japan was never able to achieve its tourism goal of reaching 40 million visitors in 2021. Looking back on 2021, the total foreign visitor volume may only amount to roughly 30,000. While border restrictions are starting to relax to a three-day quarantine, Japan has only seen 25,900 visitors through the end of October.

With the Olympics being a made-for-TV event, Japan was never able to achieve its tourism goal of reaching 40 million visitors in 2021. Looking back on 2021, the total foreign visitor volume may only amount to roughly 30,000. While border restrictions are starting to relax to a three-day quarantine, Japan has only seen 25,900 visitors through the end of October.

Japan has a new prime minister, Fumio Kishida (l.), who recently just secured the hold that his party, the Liberal Democratic Party, has on the Lower House of the Diet that will ensure that IRs remain on track as the country begins to loosen its restrictions from the Great Shutdown.

Japan, which has one of the highest vaccination rates in the world, will need to have IRs become a catalyst as it looks to restore and build upon its pre-pandemic tourist volumes. With the Olympics in the rearview, IRs remain the single biggest opportunity for tourism and further investment in the country.

The concept of IRs began to develop over 20 years ago, and 2022 presents itself as the year for meaningful progress in the market to begin the building and procurement for these iconic structures that will become economic engines for the country. The question that remains is how the three current frontrunners to host IRs will get their process to the finish line.

As the new year begins, the three current finalists of Osaka, Wakayama and Nagasaki are assembling their area development plans that are due in April 2022. This is now six months behind schedule from the original deadline because of the pandemic that continues to be a menace across the world, among economies that remain shuttered as well as those that are reopening.

At the beginning of 2020, no one likely would have foreseen these three cities as the finalists for the three initial licenses in Japan. Heading into 2022, the question becomes whether all three will be chosen in the end. The overall process became much less driven after the demise of Yokohama’s initiatives, which left investment and tax revenue on the table without having an IR in the Kanto region, the largest and most heavily populated in Japan.

The Tokyo metro area continues to offer the most interesting potential opportunity as Japan’s largest population center, but remains out of the mix. This also leaves out several top-tier operators that had an interest in the Kanto region but either opted out of the Yokohama market or were left behind in the process as it fell apart in August 2021. One of the biggest questions is whether these operators such as Genting, Melco, Galaxy, Las Vegas Sands or Wynn are able to get back into the race should another site become available.

Osaka and its partnership between MGM Resorts and Orix seem to be set for approval. In Nagasaki, the process had narrowed to achieve their selection in Casinos Austria, and there is now a potential fallout from the two losing bids and their claims against a fair process. On the other hand, Wakayama, which is located in the neighboring prefecture to Osaka, surprised many earlier in 2021 with the announcement of Caesars as a partner.

Not only was this a surprise as Caesars had taken international development out of the mix previously, but it brought further legitimacy to the Wakayama bid by having a world-renowned brand along with a solid team in Global Gaming Asset Management and Clairvest.

The Japan opportunity still poses some risks as the market rolls out into the future. With the current state of geopolitical dynamics that are associated with the market, it remains to be seen whether the market will reach its potential when the first IRs open in 2027 or beyond. The pandemic continues to take its toll on the global economy, but the longer lasting geopolitical climate, specifically in Asia, makes this more interesting.

Next year looks as though Japan will finally reach its first milestone in the selection of licensees. Japan remains the best announced market opportunity for the gaming industry. While the market still has its challenges ahead, the opportunity for the next phase of integrated resorts remains strong. While questions remain on whether all three current contenders will be chosen or if there will be opportunities for others to enter, look for 2022 to be the next chapter as gaming finally starts to move forward in the land of the rising sun.

—Brendan D. Bussmann is a partner and director of government affairs with Global Market Advisors (GMA).

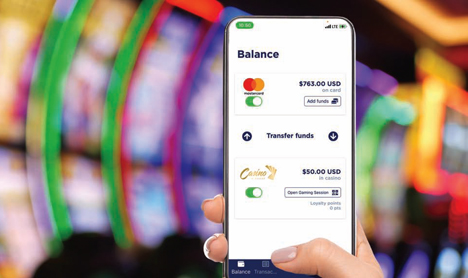

9. Breezing Toward Cashless

When it comes to casinos and technology, the regulatory community hasn’t always been the most expedient.

When it comes to casinos and technology, the regulatory community hasn’t always been the most expedient.

For years after slot machines went digital, the queue in state-operated approval labs was ridiculously long; it took the advent of private labs to solve that problem. When cash has been involved, there also is a history of cautious regulation—many jurisdictions outlawed ATM machines on casino floors, for instance.

However, when it comes to removing cash-handling from casino floors, the opposite has been true. Twenty years ago, the removal of coins from slot machines happened with blinding speed as regulators swiftly approved ticket-in/ticket-out technology.

Now, the removal of cash as the primary method of payment on the casino floor looks like it will occur just as smoothly. Operators and casino customers have been anxious to put systems in place to enable cashless and contactless payment options on the casino floor since the pandemic lent new urgency to the goal. Suppliers of cashless technology report that the regulatory community has recognized the need to implement cashless options as well, and so far, applying new cashless technology in casinos has been, from a regulatory standpoint, smooth sailing.

“IGT’s experience with regulators as it relates to the advancement of cashless gaming has been overwhelmingly positive and collaborative,” says Ryan Reddy, the supplier’s senior vice president of global product management for VLT, poker, systems and payments.

“They recognize and embrace the value of future-forward technologies such as Resort Wallet and IGTPay, and are committed to facilitating opportunities to responsibly introduce these products in casinos.” IGT is rapidly deploying its digital wallet system and payment gateway to customers using the IGT Advantage casino management system.

Acres Manufacturing has experienced similar regulatory smooth sailing with its Acres Wallet product, which works within the Foundation CMS and interfaces with other CMS products to add cashless functionality.

“Acres Manufacturing is currently working on cashless deployment with regulatory bodies in 11 states,” says Noah Acres, chief operating officer of Acres Manufacturing. “To date, regulators have been extremely enthusiastic, helpful and accommodating on this issue.

“Governments love cashless gaming because everything can be tracked, and that has major implications on issues ranging from accounting to problem gambling. I feel confident that casinos nationwide will be able to offer players a convenient and fun cashless experience in the very near future. Cashless is something wanted by everyone—players, operators and regulators.”

“The rise of cashless solutions in the industry inevitably increases the risk of fraudulent behavior, creating the need for strong account-level security and anti-money laundering (AML) practices,” agrees Christopher Justice, president of Global Payments Gaming Solutions. “As an industry leader, Global Payments answered that call by engineering VIP Mobility to provide additional layers of consumer protection at the game and elsewhere while working within existing gaming regulations to provide the most secure cashless ecosystem in the industry.”

If there is one trend to identify with respect to the advent of cashless gaming, it is that its adoption promises to accelerate in 2022.

“I anticipate we’ll see continued expansion of cashless gaming in 2022, especially as gaming operators in major gaming markets such as Nevada deploy it more widely,” says Reddy. “IGT has several exciting deployments scheduled in multiple states for H1 2022, and we have been aligned with regulatory entities throughout the process of implementing our solutions.”

—Frank Legato

10. The Great Resignation

The pandemic had many impacts on gaming, but the most insidious has been the difficulty in bringing back your employees and replacing those who didn’t come back. It’s an issue that’s not specific to the casino industry, but it’s one that is difficult to solve and remains a drag on the recovery from Covid-19.

The pandemic had many impacts on gaming, but the most insidious has been the difficulty in bringing back your employees and replacing those who didn’t come back. It’s an issue that’s not specific to the casino industry, but it’s one that is difficult to solve and remains a drag on the recovery from Covid-19.

Dubbed by the media as the “Great Resignation,” the employment crisis is real and growing more desperate by the day.

John Ceresani is a principal at the Pharos Group, a human resources consulting group with many gaming industry clients. A former HR executive at the Claridge and Caesars Atlantic City, he recognizes the problem is complex.

“It’s a challenge,” he says, “but it’s no different than any other industry. The pandemic has brought up a lot of psychological issues with workers that have changed the way people look at the workplace.”

With casino closures starting at a minimum of three months and stretching even today to almost two years, Ceresani says the individual workers may all have different reasons on whether they return to work.

“The numbers of people who have left the workplace without getting another job is astounding,” he says. “It comes down to how they felt about the place they worked prior to the pandemic. Did they value their people? Was it a great working environment? If you were on the right side of that, maybe you didn’t get hurt so badly. Your employees would have had a positive feeling about going back. But if they weren’t, and they had a chance to get a time-out during these very difficult times, maybe they don’t want to go back. When you’re working 60-70 hours a week you don’t have time to reflect on what might be better for you, but now you’ve had a chance to see what life was like without that stress. Maybe it’s not what you want anymore.”

Ceresani says the time to think also stirred ideas of self-sufficiency. Whether it’s stepping back and figuring out how to retire at an earlier age, or taking the chance to build a business on their own, it also played a part in the decision to return to work or not.

“People retiring at an early age is also a reality now,” he says. “And some of them are starting their own businesses, finding a niche in their own world. Maybe they thought their talent was not valued at their workplace so now they’re going to take the shot they’ve been putting off for so long.”

Many state governments extended unemployment benefits for months even after businesses began to reopen, but Ceresani doesn’t believe that was a big factor in decisions about the workplace.

“Yes, it impacted a segment of society that figure if they can get a free ride, they’re going to take it,” he believes. “But I think a majority of folks had time off and some of their basic needs were being met, but then they started reflecting on what was important to them, and what they really needed to survive.”

But what happens when your employees begin to come back, but the effect of the pandemic lingers? Employees may begin to think there might be a better job out there, particularly when competitors are desperate for workers. What will prevent them from leaving?

“How do employers relate to folks to get them back in the workplace after they’ve gone through this?” Ceresani asks. “It’s going to take real leadership to figure out how to do this. You’ve got to convince people that your organization values them and they’re working for something bigger than themselves. Un- fortunately, the larger companies just aren’t connecting with their people.”

Older workers are more likely to consider retirement, but lots of workers who don’t return are younger. And Ceresani says there’s a reason for this.

“Millennials get a bad rap,” he insists. “They work hard, especially if they love what they’re doing. But they have to be engaged if they’re going to do it. It has to mean something to them. They’re not going to dummy up and deal, like we did in the old days.”

Many companies resorted to bonus offers for new employees, and Ceresani says that’s a viable strategy but needs to be just part of an overall plan.

“Bonuses aren’t going away anytime soon,” he says. “That’s the natural tendency to look at money as the solution. It’s part of the short-term solution for sure. You want to get people to come in and start to work. The challenge is making them stay. Sure, you can bribe people to take a job, but if they hate that job, it’s not going to work in the long run. That’s the danger for employers. Turnover costs money.

“There should be a strategy about how you bring them in and connect them to something they can appreciate. Enlightened companies will appreciate their employees and treat them very well.”

But if you didn’t consider your employees’ needs during the pandemic, you might be playing catch-up, says Ceresani.

“During the pandemic, the Hard Rock in Atlantic City showed their employees they were valued by giving them something to help them get by—gift cards for groceries, and other things. They were thinking ahead to these problems. Casinos that didn’t recognize that these problems were happening probably didn’t do so well in bringing their people back.”

—Roger Gros